Monthly Market Wrap May 2026

The Signal in the Noise: Structure Holds When Markets Don't Agree

This past week offered a masterclass in market indecision. Mainstream equities marched higher, while Bitcoin consolidated, struggling to break through its recent resistance levels. It is a moment that rewards clarity over reaction, reminding investors that true resilience comes from structure, the kind that lets an allocation hold firm when headlines don't quite align.

News Digest

This week's developments focused on regulation and institutional activity, both of which continue to shape the digital asset market.

The SEC approved Paxos as a blockchain-based clearing agency. This decision supports the use of blockchain technology in traditional financial services and may encourage further institutional participation.

In Europe, regulators continue to implement the Markets in Crypto-Assets (MiCA) framework. UniCredit raised concerns about how banks may handle future crypto-related risks, while France's AMF set a June 30 deadline for MiCA licensing applications. These developments show that the regulatory environment is becoming clearer, although challenges remain.

Institutional interest also remained visible. Bit Digital purchased $20 million worth of Ethereum, signalling continued confidence in ETH as a long-term investment. At the same time, Fidelity Digital Assets discussed the growing role digital assets could play in a changing global financial system.

Taken together, these developments point to a market that is becoming more integrated with traditional finance and increasingly shaped by regulation and institutional participation.

The Macro Lens

Economic indicators provided a generally supportive backdrop for risk assets.

The US 10-year Treasury yield fell 3.05% to 4.455%. Lower yields can make growth-focused assets more attractive by easing financial conditions.

The Dollar Index (DXY) was largely unchanged, rising just 0.05% to 99.02. A stable dollar reduces pressure on risk assets and supports international investment flows. Gold gained 1.09% during the week. Suggesting that while investors are willing to take on risk, many still value portfolio diversification and protection against uncertainty.

Overall, the macro environment remains relatively balanced. Conditions are supportive for risk assets, but investors continue to show caution in certain areas.

The Stocks Lens

Equity markets had a strong week, propelling major indices higher. The S&P 500 climbed 1.60%, while the Nasdaq 100 gained 0.84%, and the Dow Jones rose 1.96%. This broad market rise indicates investors are feeling more confident, a sentiment that frequently spills over into digital assets.

Microsoft, an indicator of the broader tech sector, led the charge among the Magnificent Seven stocks with a healthy 5.37% gain, alongside Meta (up 3.03%) and Amazon (up 1.43%). This momentum often indicates confidence in corporate earnings and future growth prospects, encouraging capital allocation towards higher-beta assets.

Not all tech names participated in the rally equally, as Nvidia experienced a 5.13% dip, and Tesla edged down 0.71%. This selective movement within the top tech names indicates that investors are still discerning, favoring established players with immediate returns while taking profits or rotating out of those facing near-term pressures.

The VIX, commonly known as the market's "fear gauge," dropped 14.60% to 15.74. Lower volatility typically reflects stronger investor confidence and a greater willingness to invest in growth-oriented assets.

Overall, equity market performance remains supportive for risk assets, including digital assets.

The Crypto Lens

Digital assets faced a complex week, with Bitcoin consolidating around the $73,641 mark, a 4.9% weekly drawdown. Ethereum mirrored this pattern, slipping 5.6% over the week to $2,012.48, though it did show a stronger 2.0% daily recovery compared to Bitcoin's 1.2% gain.

The ETH/BTC ratio, currently at 0.0273, reflecting Bitcoin's continued strength relative to the broader crypto market. During periods of uncertainty, investors often favour Bitcoin over smaller digital assets.

Market sentiment remains cautious. The Fear & Greed Index registered a score of 23, firmly in "Extreme Fear," which stands in stark contrast to the "Greed" observed in traditional equities. This divergence highlights that while macro sentiment is improving, digital asset investors are still processing recent volatility.

The total crypto market cap stands at $2.56 trillion, with stablecoin market cap at $289.6 billion, suggesting that a significant pool of capital remains on the sidelines, ready to be deployed should sentiment shift.

This week reinforced the value of maintaining a long-term investment plan rather than reacting to short-term market movements.

The ICONOMI Angle

Periods where stock markets and crypto markets move in different directions can test investor confidence. They can also highlight the importance of having a clear investment strategy.

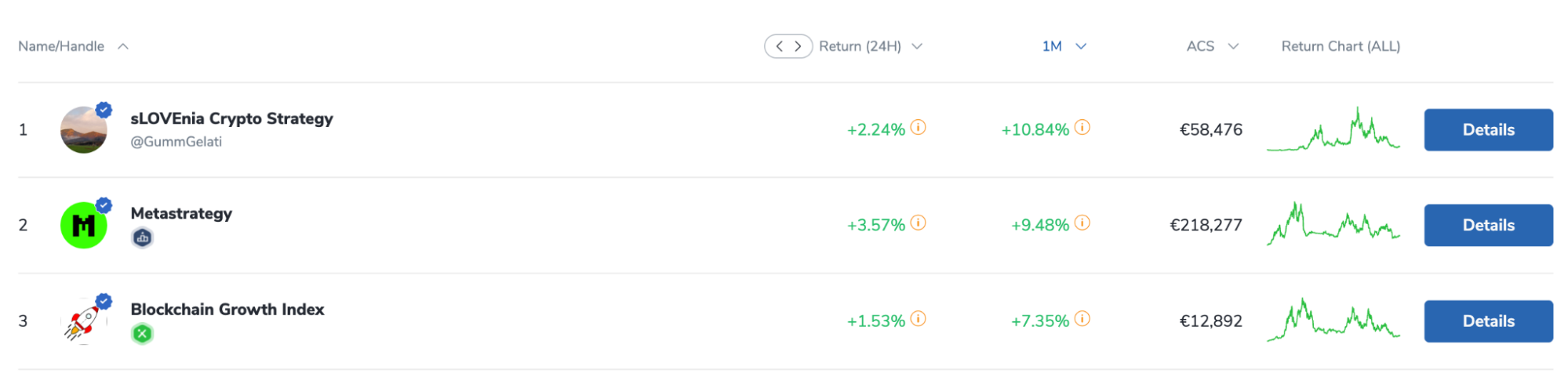

Our top-performing strategies this month demonstrate this resilience. sLOVEnia Crypto Strategy, for instance, delivered a robust 10.84% return over 30 days, even with a smaller AUM. Its top holdings, including ENA, FXS, and INJ, show a focus on specific, high-conviction assets that outperformed the broader market. Metastrategy also delivered 9.48% for the month, leveraging assets like INJ, BTC, and NEAR.

What these results tell us is that systematic portfolio management, which removes the emotional decision-making from volatile periods, is not just theoretical; it delivers during times of market indecision.

For investors concerned about market noise, these performances underscore that discipline is structural, and that disciplined allocation continues to work through the noise rather than needing perfect conditions.

The Month Ahead

June 10: U.S CPI for May 2026. The release covers May 2026 inflation and is a major macro catalyst for crypto and risk assets.

June 15 - 17: G7 Summit in Évian, France. While not directly crypto-focused, discussions around global financial stability and digital currencies could influence regulatory sentiment.

June 30: France AMF MiCA Licensing Deadline. Crypto firms operating in France must secure their MiCA licenses, which may lead to consolidation or clarity within the French crypto market.

What to Watch Next

Investor Behavior vs. Market Sentiment: Will the “Extreme Fear” in crypto persist even as traditional markets push higher, or will retail investors start to re-engage?

Regulatory Momentum: How will MiCA implementation across Europe unfold, and will the SEC's recent actions signal a broader trend of blockchain integration?

Institutional Flow Continuity: Continue watching for significant institutional purchases like Bit Digital's Ethereum acquisition, as these can provide a sustained floor for asset prices.

DXY and 10Y Yield Stability: Any sudden shifts in these macro indicators could quickly alter risk appetite across equity and digital asset markets.

FAQs

Why are traditional markets showing signs of greed while crypto is in extreme fear?

This divergence shows different investor psychology in play. Stock markets are buoyed by strong earnings and falling VIX, while crypto investors might still be processing recent volatility, creating a moment where structured allocation can separate from short-term sentiment.

How does SEC approval of Paxos affect my digital asset portfolio?

The SEC's approval of Paxos as a blockchain-native clearing agency enhances the legitimacy and efficiency of blockchain technology in finance. This development could attract more mainstream investment into digital assets, benefiting diversified portfolios with exposure to this maturing sector.

Should I adjust my portfolio based on the recent stock market rally?

The equity rally indicates a broad 'risk-on' sentiment, but panic-buying might be unwise. Your portfolio's structure was designed for periods of market discrepancy, rewarding a disciplined approach rather than reactive adjustments driven by short-term market noise.

Ready to start your journey with us?

Trusted by over 100,000 users from around the world.